There is a system running at the foundation of global trade that most people have never heard of. It is not secret. It is not a conspiracy. It is the outcome of a specific historical sequence — a world war, a currency crisis, a diplomatic negotiation, and fifty years of compounding economic inertia — and it shapes the price of everything you buy, the interest rate on your mortgage, the strength of your paycheck, and the long-term value of every asset you own.

It is called the petrodollar system.

Understanding it is not optional for anyone serious about money. It is the reason the United States can run deficits that would collapse any other currency. It is the reason gold behaves the way it does. It is the reason sanctions work. And it is the reason the working class in every oil-importing country on earth is, without knowing it, quietly subsidizing American government spending every single day.

This is not a story about oil. It is a story about power, architecture, and who pays the bill.

Act I: How the Dollar Became the World's Money

Bretton Woods, 1944

In July 1944, with World War II still being fought, 730 delegates from 44 Allied nations gathered at the Mount Washington Hotel in Bretton Woods, New Hampshire to answer one question: how do you rebuild a global trading system from rubble?

The answer required a single anchor currency — one that the world could trust, settle trade in, and hold as a reserve. The selection was not arbitrary. The United States controlled approximately two-thirds of the world's above-ground gold supply. Its industrial base was intact. Its government was stable. Every other candidate had been disqualified by the war.

The Bretton Woods agreement fixed the dollar to gold at $35 per ounce. Every other currency then pegged to the dollar. The dollar was the only currency foreign central banks could redeem for physical gold on demand. The IMF and World Bank were born at the same conference. In a single week of negotiations, the U.S. dollar was formally installed as the axis of the global financial system - not by conquest, but by economic logic.

There was one dissenting voice worth knowing. John Maynard Keynes, representing Britain, proposed a different arrangement entirely - a supranational currency he called the "bancor", issued by an international clearing union, belonging to no single nation. Keynes understood, with precision, what making the dollar the reserve currency would mean: an enormous, permanent structural advantage for the United States that no other country would ever share. He lost the argument. The American delegation insisted on the dollar. Keynes's prediction about the advantage proved exactly right.

The Triffin Dilemma — The Built-In Contradiction

In 1960, economist Robert Triffin identified a fatal structural flaw in the Bretton Woods system. For the rest of the world to hold dollar reserves — to use them, accumulate them, settle trade in them — the United States had to supply dollars to the world. The only way to supply dollars to the world was to run a balance-of-payments deficit: spend more abroad than came back. But if the U.S. ran persistent deficits, foreign nations would accumulate more dollar claims than the U.S. gold reserve could back, eventually destroying confidence in the gold-dollar peg.

This is the Triffin Dilemma: to be the world's reserve currency, you must run deficits. But running deficits eventually destroys confidence in your currency. There is no clean solution. The issuer of the global reserve currency is structurally required to consume more than it produces - forever.

Triffin published this in 1960. The system collapsed in 1971. He was right about the mechanism. It just took longer than he expected.

The Nixon Shock — August 15, 1971

By 1971, the arithmetic had become impossible. The Vietnam War was hemorrhaging dollars. The Great Society programs were expanding domestic spending. The Federal Reserve was running loose monetary policy. Dollars were flooding out of the United States faster than gold was coming in.

France under de Gaulle had been particularly aggressive about exercising its right to exchange dollars for gold. De Gaulle's Finance Minister, Valéry Giscard d'Estaing, had given the arrangement a name: "the exorbitant privilege". France reportedly dispatched its navy to New York to collect its gold. By 1971, the United States held roughly $10 billion in gold against approximately $80 billion in dollar liabilities to foreign central banks. The peg was indefensible.

On the evening of August 15, 1971, Nixon interrupted regular television programming — the show was Bonanza — to announce that the United States was immediately suspending the convertibility of dollars into gold. Bretton Woods was over.

This is where popular finance content almost universally gets the story wrong. The Nixon Shock did not create the petrodollar system. What it created was a structural crisis: the dollar now had no commodity anchor. The world had been holding dollars because they were as good as gold. Now they were backed by nothing but the credibility of the U.S. government and the inertia of existing trade patterns. Something had to replace gold as the reason the world would continue to hold and transact in dollars. Two years later, a war in the Middle East provided the answer.

Sponsored Video

Act II: The Deal That Wasn't — And the One That Was

The 1973 Oil Embargo

On October 6, 1973, Egypt and Syria launched a coordinated offensive against Israeli-occupied territory. Nixon authorized a massive U.S. resupply operation to Israel. In response, the Arab members of OPEC declared an oil embargo against the United States and other countries supporting Israel. Oil quadrupled from approximately $3 per barrel to nearly $12 per barrel in months. American gas stations ran dry. Lines stretched for miles. States imposed odd-even license plate rationing.

The vulnerability was total and undeniable. Every oil-importing economy had just learned in real time that oil was not merely a commodity. It was a weapon. The country that controlled oil supply held a gun at the throat of the modern economy. Washington understood it needed to make sure that gun was never pointed at America again.

The 1974 Agreement — What Actually Happened

This is the most misrepresented episode in all of petrodollar history, and getting it right matters — because the myth distorts how investors and citizens understand the system.

The popular version goes like this: In 1974, the United States made a deal with Saudi Arabia — oil would only be sold in dollars, in exchange for U.S. military protection. This became the foundation of the petrodollar system.

This is inaccurate.

The agreement signed on June 8, 1974, between Secretary of State Henry Kissinger and Prince Fahd was the U.S.-Saudi Arabian Joint Commission on Economic Cooperation. It focused on economic development, technology transfer, infrastructure investment, and how Saudi Arabia would invest its oil windfall. It said nothing about exclusive dollar pricing. Saudi Arabia continued accepting British sterling for oil after signing it. The "oil only in dollars" framing is, as UBS chief economist Paul Donovan has bluntly stated, "fake news".

What actually mattered was a separate, secret agreement reached in late 1974. Its existence was not publicly revealed until 2016, when Bloomberg News filed a Freedom of Information Act request with the National Archives. This agreement was the real financial architecture: Saudi Arabia agreed to invest billions of dollars of its oil revenues specifically into U.S. Treasury securities. In exchange, the United States promised military protection, equipment, and a security guarantee for the kingdom.

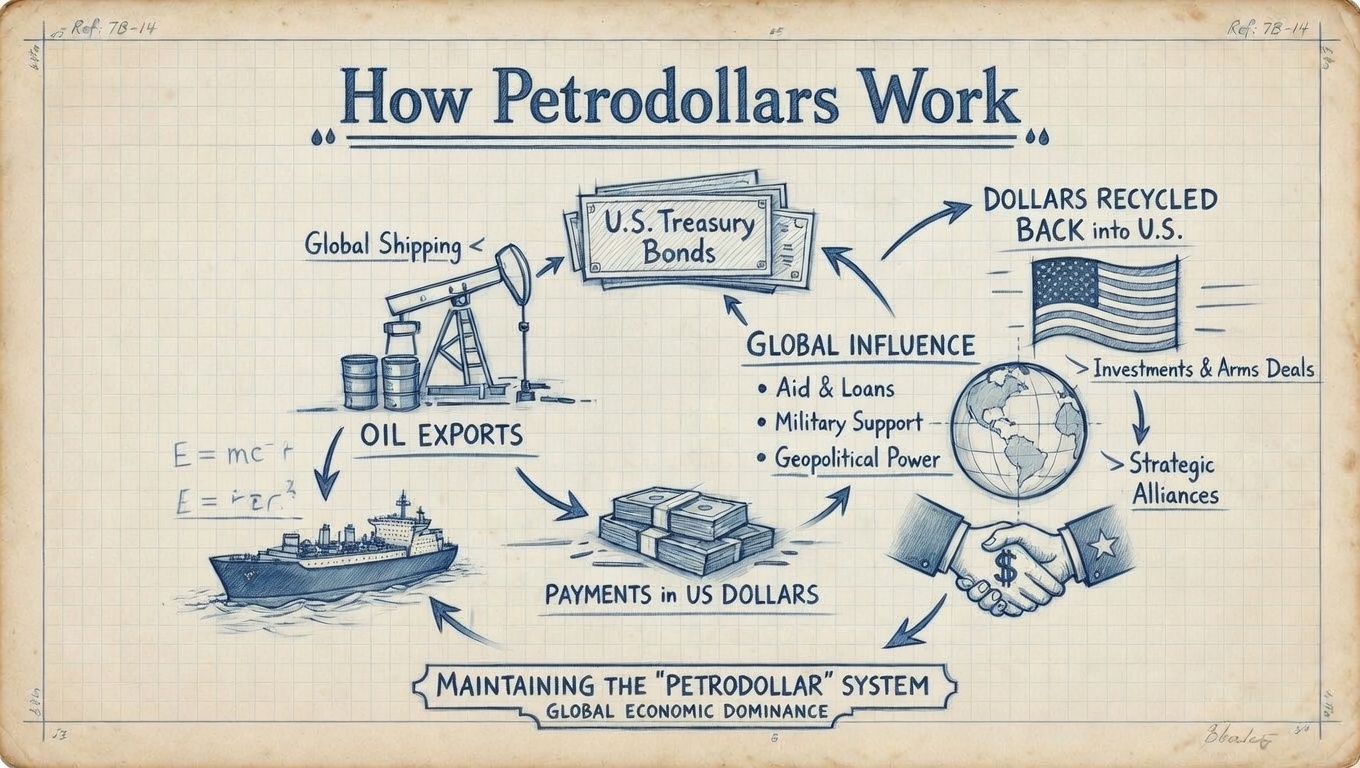

This distinction is everything. The deal that shaped the world was not about how oil was priced. It was about where the money went afterward. Saudi Arabia would earn dollars selling oil, then recycle those dollars back into the U.S. financial system by purchasing American government debt. Other OPEC members followed — not because of any formal agreement forcing them, but because the dollar was already the most liquid, most trusted, most deeply embedded currency in global trade. The network effects made switching more expensive than maintaining the status quo. Organic inertia, not coercion, is what actually sustains the system.

Act III: How the Machine Works

The Mechanism — Why Every Country on Earth Needs Dollars

Once oil is predominantly priced and settled in dollars, a chain reaction runs through the entire global economy. The logic is simple and its consequences are enormous:

Step 1: Japan, India, South Korea, Germany — every major industrial economy without sufficient domestic oil production — must buy oil on global markets. To do so, they need U.S. dollars.

Step 2: To ensure they can always buy oil without being caught off guard by currency fluctuations, every central bank maintains dollar reserves. This is not optional for any economy that imports energy.

Step 3: The safest, most liquid place to park dollar reserves is U.S. Treasury securities. So foreign central banks park hundreds of billions in American government debt — not because they love Washington, but because it is the most practical option available.

Step 4: That permanent structural demand for U.S. Treasuries suppresses American borrowing costs. The U.S. government borrows more cheaply than any other nation on earth — not because it is the most fiscally responsible, but because the world has no choice but to hold its debt.

This loop — buy oil in dollars, hold dollar reserves, park reserves in Treasuries — creates the exorbitant privilege that Giscard d'Estaing identified in the 1960s. As economist Barry Eichengreen summarized it: printing a $100 bill costs the U.S. Bureau of Engraving a few cents. Every other country that wants one has to provide $100 worth of real goods and services to obtain it.

The Concrete Advantages — What "Exorbitant Privilege" Actually Means in Practice

This is not abstract monetary theory. The advantages are measurable and they compound daily:

Cheaper borrowing. Foreign central banks buy U.S. Treasuries regardless of yield because they need dollar reserves. That artificial demand suppresses U.S. interest rates — by some estimates, by 50 to 100 basis points. On $30 trillion of national debt, that differential is worth hundreds of billions of dollars per year in reduced interest payments. Every American benefits marginally from this. The government benefits enormously.

Import discounts. A strong dollar — sustained by artificial global demand — means American consumers pay subsidized prices for imported goods. Your electronics, your clothes, your furniture: all cheaper because the world's need for dollars inflates purchasing power for anyone holding them.

Sanction power. Because virtually every international transaction of consequence clears through dollar-denominated systems, the U.S. can effectively cut countries off from the global economy without firing a shot. When the U.S. froze approximately $300 billion of Russia's foreign currency reserves in 2022, it demonstrated this power with unprecedented clarity. No other country on earth has this weapon.

No balance-of-payments crisis — regardless of deficits. Any other country running America's trade deficits would face a currency collapse within years. The U.S. does not — because those deficits are automatically financed by countries that must hold dollars anyway. The Triffin burden becomes a free pass.

Petrodollar Recycling — The Loop That Sustains Itself

When Saudi Arabia, the UAE, Kuwait, or Norway receive billions in oil revenues, they do not store paper cash in a vault. They invest it. This process — petrodollar recycling — is the mechanism through which oil wealth flows back into the U.S. financial system and amplifies the privilege.

The channels are direct and significant: purchases of U.S. Treasury securities, equity stakes in American companies, prime commercial and residential real estate in New York and London, and positions in global stock markets through sovereign wealth funds. Norway's Government Pension Fund Global — the world's largest sovereign wealth fund at over $1.7 trillion — is itself a product of petrodollar recycling, now invested across global equities.

The loop is self-reinforcing: countries buy oil in dollars, oil producers earn dollars, oil producers invest dollars back into U.S. assets, dollar demand stays elevated, borrowing costs stay suppressed, the privilege perpetuates itself. Buffett's concept of the moat — a durable competitive advantage that compounds over time — applies to monetary systems as much as to businesses. The petrodollar has the deepest moat in financial history: 50 years of infrastructure, contracts, legal frameworks, and network effects.

Act IV: The Exorbitant Burden — Who Actually Pays

This is the section that almost no financial content bothers to write. The privilege is well documented. The burden is not.

The working class in every oil-importing country pays a petrodollar tax on every transaction. Here is how it works: every time a Japanese company buys oil, a Korean factory imports crude, or an Indian power plant purchases fuel, the transaction flows through dollar systems. Banks, brokers, and clearing institutions in that chain charge fees for currency conversion, dollar clearing, and dollar-denominated settlement. Those costs flow through supply chains and land, ultimately, on the price of goods purchased by ordinary people around the world. It is a small, invisible, perpetual toll — collected by financial institutions that sit in the middle of the dollar system.

American manufacturing workers paid the steepest price of all. A strong dollar — artificially inflated by global reserve demand — makes American exports expensive and imports cheap. This is great for American consumers buying foreign goods. It is devastating for the factory worker in Ohio competing with a Chinese worker whose government can hold its currency weak precisely because it is not the reserve currency. The United States has run a trade deficit in goods in virtually every year since 1976. The communities that bore the cost of deindustrialization — the Rust Belt, manufacturing towns across the Midwest — paid the real-world price for a privilege that primarily benefited Wall Street, the federal government, and anyone who owned financial assets.

Buffett has identified this dynamic plainly, calling it the "Squanderville" problem in his 2003 Berkshire letter. A nation that consistently consumes more than it produces — financed by selling IOUs to the world — is gradually transferring ownership of its productive assets to foreign hands. The privilege lets politicians avoid the hard choices that trade deficits would otherwise force. The cost is diffused across decades and borne disproportionately by the people least positioned to hold financial assets as a hedge.

The investor class holds stocks, real estate, and other assets that float upward with dollar-driven liquidity. The working class holds their labor — the one asset that gets cheaper every time the strong dollar incentivizes offshoring.

This is not an accident. It is the arithmetic of reserve currency status — and it is why understanding the petrodollar is inseparable from understanding why wealth is distributed the way it is.

Act V: Is De-Dollarization Real? — The Data, Not the YouTube

Before discussing whether the petrodollar system is under threat, you need the actual numbers.

The U.S. dollar's share of global foreign exchange reserves has declined from approximately 71% in 2001 to approximately 57% in 2024, according to IMF COFER data. That is a real and meaningful decline over 23 years. It is not a collapse. For context:

The euro sits at approximately 21% of global reserves — essentially unchanged from its 1999 launch despite decades of predictions it would rival the dollar.

The Chinese renminbi holds approximately 2% of global reserves — despite years of aggressive Chinese promotion and enormous bilateral trade volumes.

The dollar's share of global trade invoicing is approximately 54%.

Approximately 88% of all foreign exchange transactions involve the dollar on one side.

The dollar is less dominant than it was in 2001. It is nowhere near being replaced.

Why Countries Hostile to the U.S. Still Use the Dollar

This is the question that YouTube finance consistently fails to answer seriously. If Russia wants dollar-free trade and China wants to displace U.S. hegemony, why do international oil contracts still predominantly settle in dollars?

The answer is not political loyalty. It is liquidity, infrastructure, and switching costs.

The dollar market is the deepest, most liquid financial market in human history. You can move billions without materially moving the exchange rate. The renminbi market is a fraction of the size and subject to capital controls that prevent the free movement that global trade requires. Decades of dollar-denominated contracts have also built an enormous ecosystem: derivative markets for hedging, insurance products, legal frameworks, counterparty relationships, clearing mechanisms. Switching currencies means rebuilding all of it. The cost is extraordinary.

Think of it this way: the dollar is the world's operating system. Switching to a new one is not impossible — but it requires every application, every file, every process to be rebuilt from scratch. Nobody migrates away from an operating system they depend on unless the alternative is so obviously superior that the pain of switching is worth it. No alternative currently meets that bar.

What Russia and China are actually doing is more precise than the narrative suggests. They are reducing dollar exposure selectively — in bilateral trades, under sanctions, where dollar dependence is a specific political liability — while continuing to use it where it is operationally efficient. Russia has increased oil settlement in yuan and rubles with China. China has developed CIPS (its cross-border payment system) as a partial alternative to SWIFT. Both have been buying gold aggressively. None of this is a revolution. It is a hedge against the specific risk of dollar weaponization — not an attempt to replace the system globally.

The BRICS currency proposal deserves a blunt assessment: as of 2025, it does not exist, and the serious academic consensus is that it is unlikely in any meaningful timeframe. The BRICS bloc includes countries with wildly divergent interests, competing geopolitical rivalries (India and China share a contested border), and incompatible monetary frameworks. A shared reserve currency requires a level of political and economic integration that took Europe decades to build — and the eurozone has endured repeated existential crises even with that integration. The renminbi's 2% share of global reserves after years of active Chinese promotion illustrates precisely how hard currency internationalization actually is.

The Greatest Long-Term Threat — Self-Inflicted

The most consequential long-term risk to dollar dominance is not China's ambition or Russia's resentment. It is Washington's own overuse of financial sanctions.

When the U.S. froze approximately $300 billion of Russia's foreign reserves in 2022 — assets held in Western institutions that Russia had accumulated legally over decades — it sent an unmistakable signal to every government on earth: dollar reserves are not neutral savings. They are potential hostages. Any country that might one day face U.S. sanctions now has a direct, concrete incentive to hold fewer dollar assets.

Central bank gold purchases hit record highs in 2022 and 2023, driven heavily by emerging market central banks diversifying away from an asset that demonstrated it could be confiscated by political decision. The exorbitant privilege, used too aggressively, erodes the trust it depends on. The moat is being drained — slowly, measurably, from the inside.

Act VI: The Intelligent Investor's Action Plan

Understanding the petrodollar is not an academic exercise. It has direct, concrete implications for how you build and protect wealth. Here is the playbook — not a vague "scenario table," a real action plan.

Action 1: Recognize the Dollar Bias in Your Portfolio — and Decide If It's Intentional

If you are primarily invested in U.S. equities, U.S. bonds, and dollar cash, you are making an enormous implicit bet on continued dollar dominance. That bet has paid off for decades. It is not guaranteed to pay off forever.

This does not mean panic-diversify. It means be deliberate. Know that you are making this bet. Understand the conditions under which it stops working. And size your position accordingly.

Recommended check: What percentage of your portfolio is denominated in dollars? If the answer is 100%, ask yourself whether that is a conscious decision or simply inertia.

Action 2: Hold Gold as a Monetary Architecture Hedge — Not as a Crisis Trade

The petrodollar framework clarifies precisely why gold behaves the way it does. Gold is not primarily a geopolitical crisis hedge — the 1990 Gulf War proved that. Gold is a monetary architecture hedge. It performs when:

Central banks are adding gold to reserves, diversifying away from dollar assets

Real interest rates are low or negative (the opportunity cost of holding gold is low)

Dollar dominance is structurally questioned, not just temporarily stressed

The record central bank gold buying in 2022–2024 is not a panic trade. It is a direct, measured response to the weaponization of dollar reserves. That is a structural signal, not a short-term one. Our standing position remains: 0–5% gold maximum, only if you believe the Fed stays accommodative. But the reason to own it — if you own it — is monetary architecture risk, not oil prices or war headlines.

Do not buy gold because you watched a YouTube video about the dollar collapsing. Buy it if you have a coherent thesis about the Fed's monetary policy direction and the pace of de-dollarization. Those are different things.

Action 3: Watch These Three Signals for Dollar Structural Stress

The petrodollar system will not end with a bang. It will erode gradually. Here are the indicators that the erosion is accelerating:

Signal 1 — IMF COFER Dollar Reserve Share. Track this quarterly. Currently ~57%. If it breaks below 50% meaningfully and sustains, that is a structural shift worth repositioning around. A slow drift from 57% to 55% over two years is noise. A sustained fall below 50% is a regime change.

Signal 2 — Central Bank Gold Purchases. If central banks outside the West continue buying gold at 2022–2023 levels or accelerate, it means the dollar weaponization lesson is being structurally internalized — not forgotten. Watch the World Gold Council's quarterly central bank demand data.

Signal 3 — U.S. Sanction Overreach. Every new major sovereign asset freeze accelerates de-dollarization. This is the variable Washington controls and consistently mismanages. Watch it.

Action 4: Understand That U.S. Deficits Are Structurally Different — Do Not Extrapolate to Other Currencies

The petrodollar is why the U.S. can run deficits that would destroy any other currency. This has two implications for investors:

First, do not short U.S. government bonds based on deficit arithmetic alone. The demand for Treasuries is structurally supported by reserve currency mechanics that do not apply to any other sovereign bond market. The Japanese, British, and Italian governments cannot run U.S.-style deficits without consequences. The U.S. can — until the reserve currency status erodes enough to matter.

Second, do not assume the U.S. should run these deficits. Buffett's Squanderville framing is correct: a nation that finances consumption by issuing IOUs to the world is gradually transferring ownership of its productive assets to foreign creditors. The privilege is real. The long-run cost — in hollowed-out industry, in structural trade imbalances, in growing foreign ownership of American assets — is also real. A disciplined investor accounts for both.

Action 5: The Fortress Still Holds — But Know What It Is Built On

The petrodollar system does not change the fundamental investment strategy. Wonderful businesses with durable moats, pricing power, and capital-light models outperform across every monetary regime. Coca-Cola raised its prices through the inflation of the 1970s. Visa processes transactions regardless of which currency they denominate. Johnson & Johnson sells medicine whether the dollar is at a 20-year high or a 20-year low.

What the petrodollar does change is the context:

If dollar dominance fades materially, U.S. borrowing costs will rise. That is bad for growth stocks priced on cheap debt and good for cash-generating businesses that don't need cheap capital markets to survive.

If the Fed uses the reserve currency's inflation tolerance to run persistently loose policy, real assets and productive businesses outperform cash and bonds — exactly as they did in the 1970s.

If de-dollarization accelerates, international diversification becomes more valuable — not into currencies per se, but into wonderful businesses domiciled outside the dollar zone.

None of this changes the core playbook: 85–95% productive assets, 5–15% dry powder in short T-Bills, zero long-term bonds, zero leverage, maximum patience.

The petrodollar system tells you why that playbook works. The reserve currency privilege has been quietly subsidizing the U.S. government for 50 years — and that subsidy flows through into the entire financial ecosystem that your portfolio sits in. Understanding the architecture is understanding why the rules of the game are what they are.

Conclusion: The Most Important Monetary Fact in Finance

The petrodollar is not a conspiracy. It is not a "deal" where Saudi Arabia agreed to sell oil only in dollars in exchange for military protection — that is a myth. It is the cumulative outcome of historical accidents, deliberate diplomacy, and 50 years of network effects so deep that no alternative yet offers the liquidity, legal infrastructure, and institutional trust needed to replace them.

What you now understand that most people do not:

Bretton Woods was a structural bargain — the U.S. traded currency stability for permanent monetary dominance. Keynes saw it clearly and lost.

The Nixon Shock did not create the petrodollar — it created the vacuum that the 1974 recycling arrangement filled. Dollar dominance survived gold's removal because oil and inertia replaced it.

The real 1974 deal was about recycling, not pricing — it was a secret agreement to channel Saudi oil revenues into U.S. Treasuries. The "oil in dollars only" story is factually wrong.

De-dollarization is real, gradual, and nowhere near crisis — 57% of reserves vs. 71% twenty years ago. The renminbi is at 2%. This is erosion, not revolution.

The greatest risk is self-inflicted — every dollar weaponized through sanctions accelerates the search for alternatives. The privilege is being consumed faster than it is being renewed.

The working class pays the most invisible price — through petrodollar transaction costs they never see, through deindustrialization driven by an artificially strong dollar, and through a financial system where the rules of the game have been set by the needs of reserve currency maintenance, not the interests of wage earners.

Understanding the system is how you stop being a passive participant in it — and start positioning yourself as an owner, not just a subject, of the economy it runs.