Full Transcript

Warren Buffett on the Owner's Earnings, Insurance Float & GEICO's Intrinsic Value

WARREN BUFFETT: It goes back some years on that [Owner's Earnings] description.

REMEMBER

Buffett defined the Owner's Earnings concept in the Appendix of his 1986 Letter to Shareholders:

If we think through these questions, we can gain some insights about what may be called 'owner earnings.' These represent (a) reported earnings plus (b) depreciation, depletion, amortization, and certain other non-cash charges... less (c) the average annual amount of capitalized expenditures for plant and equipment that the business requires to fully maintain its long-term competitive position and its unit volume.

Yeah. In the case of the businesses that we're in, both wholly owned and major investee companies, we regard the reported earnings — with the exception of the — some major purchase accounting adjustment, which will usually be an amortization of intangibles item — we regard the reported earnings — actually the reported earnings plus — plus or minus, but usually plus — purchase accounting adjustments, to be a pretty good representation of the real earnings of the business. Now you can make the argument that when Coca-Cola's spending a ton of money each year in marketing and advertising that they're expensing, that really a portion of that's creating an asset just as if they were building a factory, because it is creating more value for the company in the future, in addition to doing something for them in the present. And I wouldn't argue with that. But of course, that was true in the past, too. And if you'd capitalized those expenditures in those earlier years, you'd be amortizing the cost of them at the present time. I think with a relatively low inflation situation, with the kind of businesses we own, I think that reported earnings plus amortization of any — well, it's really amortization of intangibles. Other purchase accounting adjustments usually aren't that important. I would say that they give a good representation to us of owner earnings. Can you think of any exceptions in our businesses particularly, Charlie?

CHARLIE MUNGER: No. We have — after some unpleasant early experience, we have tried to avoid places where there was a lot of compulsory reinvestment just in order to stand still. But there are businesses out there that are still like that. It's just that we don't have any.

WARREN BUFFETT: Yeah. I would say that in the case of GEICO, for example, the earnings — the gain in intrinsic value — will be substantially greater than represented by the annual earnings. Whether you want to call that extra amount owner earnings or not is another question. But as we build float from that business, as long as it's represented by the same kind of policyholders that we've had in the past, there is an added element to the gain in intrinsic value that goes well beyond the reported earnings for the year. But whether you want to really think of that as earnings, or whether you just want to think of that as an increment to intrinsic value, you know, I sort of leave to you. But I would say that there's no question that in our insurance business, where our float was $20 million or so when we went into it in 1967, and where it is now, that there have been earnings, in effect, through the buildup of the float that have been above and beyond the reported earnings that we've given to you. I think our look-through earnings are — they're very rough. And we don't try to — we don't believe in carrying things out to four decimal places where, you know, we really don't know what the first digit is very well. So, I don't want — I never want you to think of them as too precise, but I think they give a good rough indication of the actual earnings that are taking place, attributable to our situation every year. And I think the pace at which they move gives you a good idea as to the progress, or the lack of progress, that we've made. The only big adjustment I would make in those is in the super-cat insurance business, we're going to have a really bad year occasionally. And you probably should take something off all of the good years, and you probably should not regard — when the bad year comes — you should not regard that as something to be projected into the future. Charlie?

CHARLIE MUNGER: No more.

WARREN BUFFETT: No more.

IMPORTANT

Buffett formally defined Owner's Earnings in the 1986 Berkshire Hathaway Annual Letter. He argued that GAAP earnings alone were insufficient to measure a business's true cash-generating power. The concept: what can the owner actually take out of the business without impairing its competitive position?

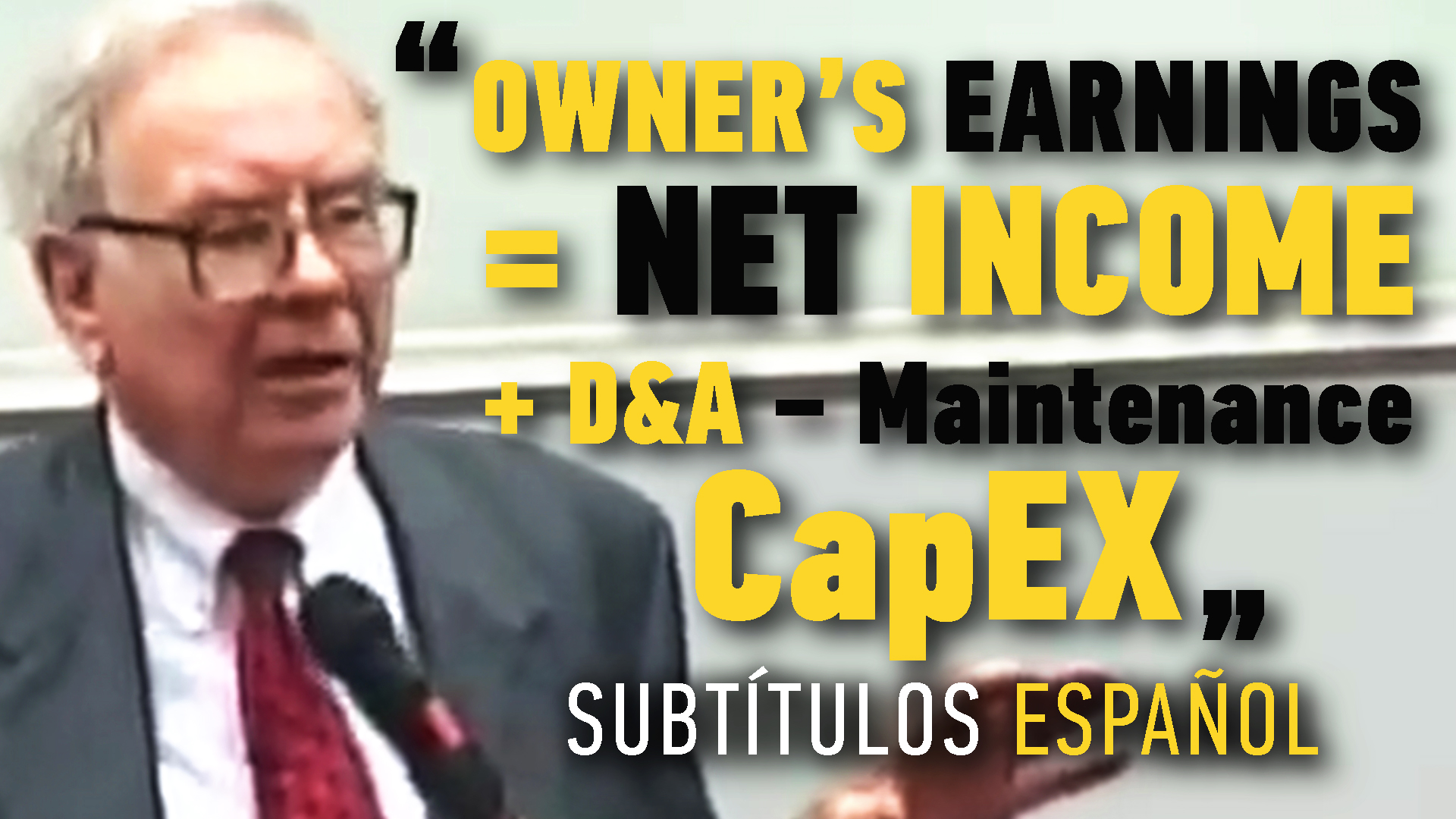

Owner's Earnings Formula (Buffett, 1986):

Owner's Earnings = Net Income − Depreciation & Amortization (D&A) − Maintenance CapEx ± Changes in Working Capital

Key distinction Owner's Yield vs. Free Cash Flow (FCF):

FCF deducts total CapEx (maintenance + growth).

Owner's Earnings deducts maintenance CapEx only.

Growth CapEx is optional investment, not an operating cost.

Key Takeaways — Owner's Earnings applied to AI's CapEx frenzy:

1. Big Tech's FCF is distorted — but not broken

Google, Meta, Amazon and Microsoft are reporting compressed FCF because the market treats $200B+ in CapEx as a cost. Buffett would ask: how much of that is maintenance and how much is growth? The core businesses — Search, AWS, Facebook — require relatively little CapEx just to keep running. Most of that spending is a growth bet, and it shouldn't penalize current Owner's Earnings.

2. The right question isn't "how much are they spending?" but "at what return?"

Growth CapEx only creates value if returns exceed the cost of capital. AWS was born from massive CapEx with extraordinary returns. The question for AI is the same: will those $200B in data centers and GPUs generate 20%+ returns or 5%? That's where the entire valuation debate lives.

3. The market is doing exactly what Buffett criticized

It's using raw "cash flow" — adding (a)+(b) without properly separating (c) — and punishing companies that actually have solid Owner's Earnings but are reinvesting aggressively for growth. Buffett called this "the cash flow fallacy" directly in the 1986 letter.

4. The real risk is CapEx that becomes maintenance

The danger with AI is that what today is growth CapEx — GPUs, data centers — becomes tomorrow's maintenance CapEx just to stay competitive. If that happens, Owner's Earnings for these companies drop structurally. That's the exact scenario Buffett and Munger always avoided — businesses requiring "compulsory reinvestment just in order to stand still."

5. GEICO vs. Big Tech — the parallel

Buffett argued that GEICO's float was building intrinsic value that never showed up in reported earnings. AI CapEx could be doing the same thing in reverse — destroying reported earnings while building strategic assets the market doesn't yet know how to value. Time will tell whether it looks more like GEICO's float or an oil company that overinvested.