Intel Corporation's stock has suffered a dramatic decline following revelations of a significant supply chain forecasting error that left the chip giant with billions in excess inventory while simultaneously failing to meet surging demand for AI-capable processors.

The Core Problem: A Historic Forecasting Failure

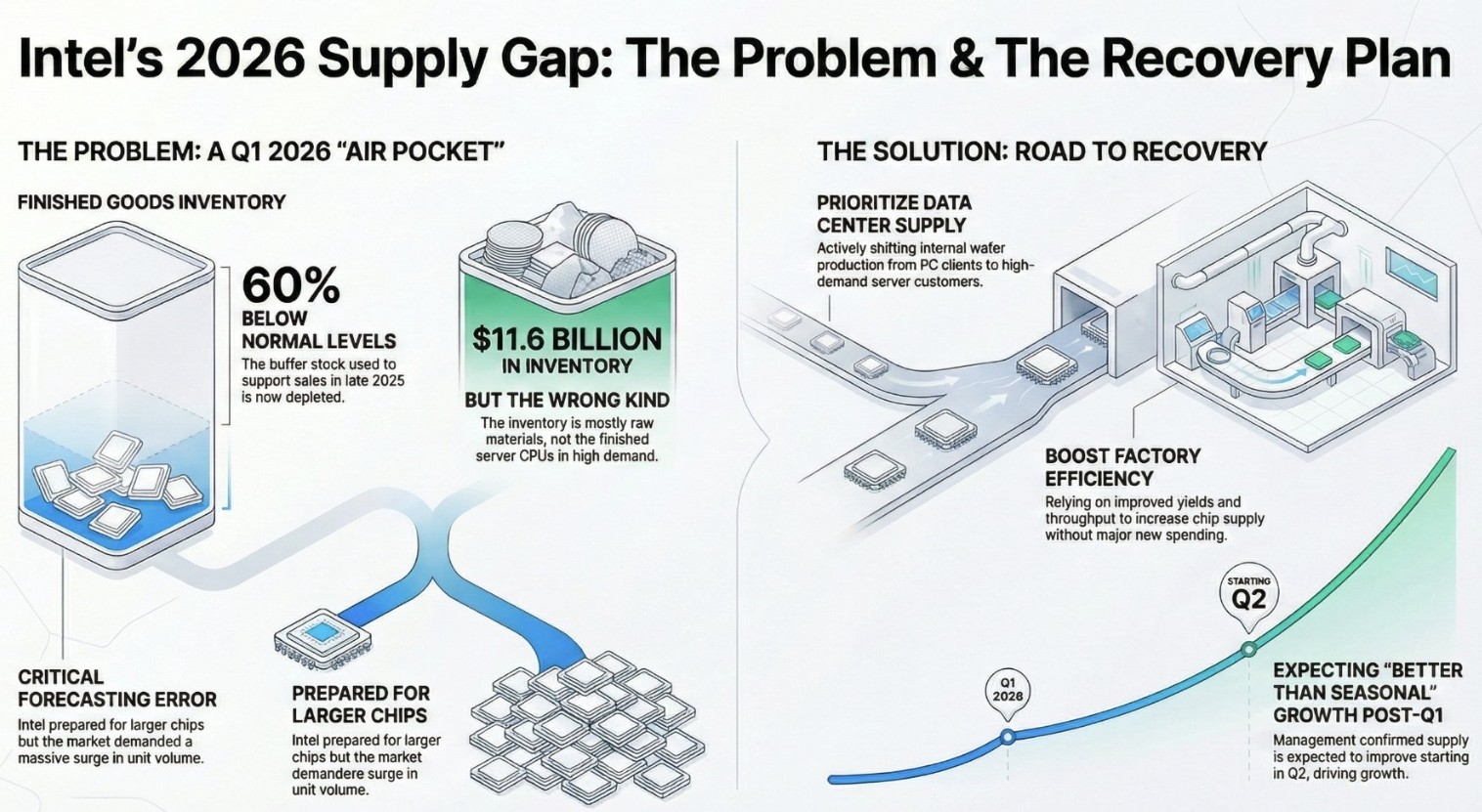

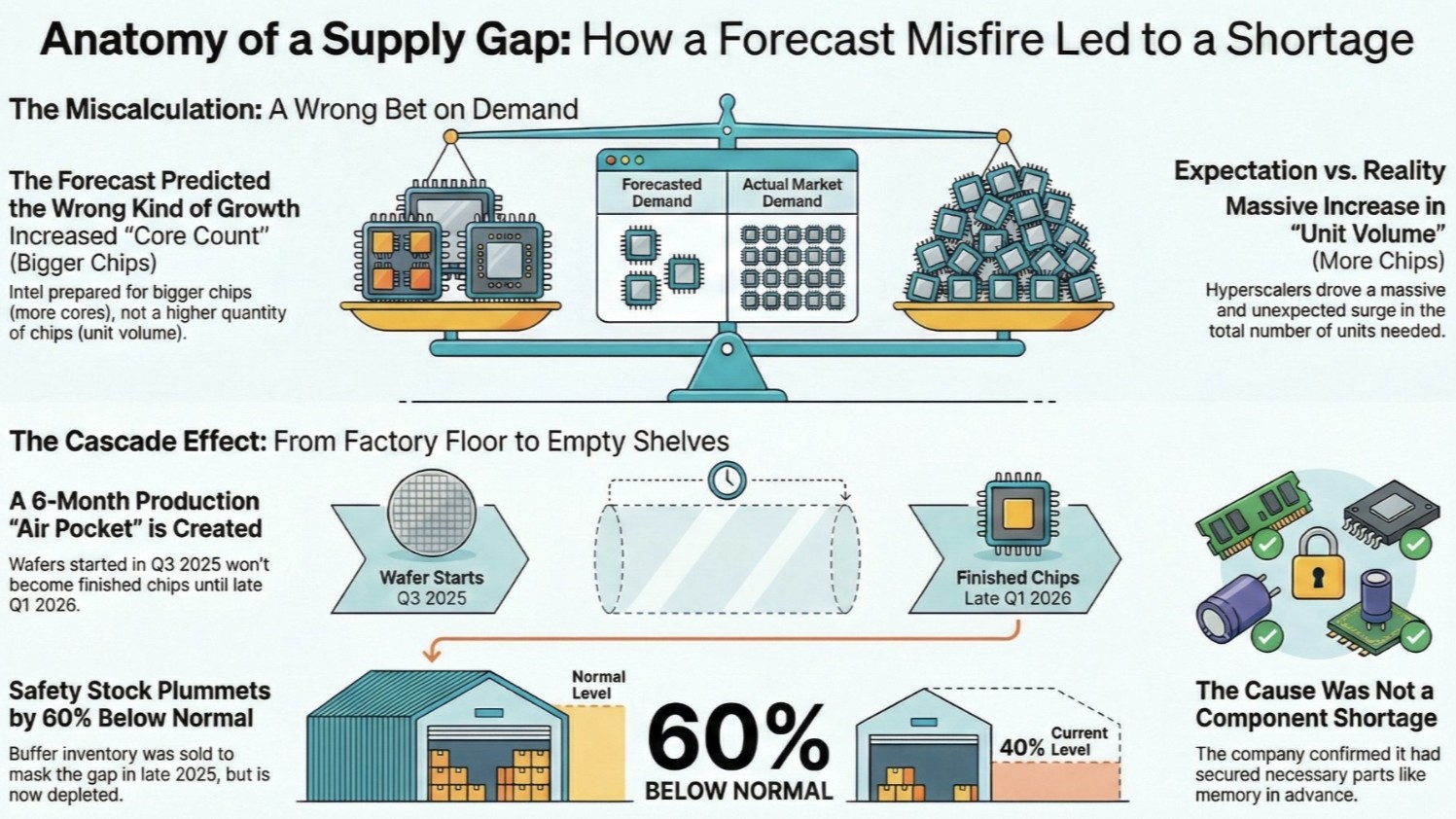

Intel's troubles stem from what analysts are calling one of the semiconductor industry's most significant demand miscalculations in recent memory. The company prepared for increased "core count"—building larger, more complex chips—when the market actually demanded a massive surge in unit volume: smaller, more numerous chips for AI data centers and hyperscale computing.

This fundamental misreading of market dynamics created what Intel executives termed an "air pocket" in Q1 2026, with finished goods inventory dropping to 60% below normal levels. Paradoxically, the company simultaneously holds approximately $11.6 billion in inventory—but it's the wrong kind. Intel stockpiled materials for larger processors while customers desperately sought the high-volume chips needed for AI workloads.

The Cascade Effect

The forecasting error has triggered a six-month production gap. Wafers that began production in Q3 2025 won't become finished chips until late Q1 2026, creating a critical supply shortage precisely when demand has accelerated. To bridge this gap, Intel depleted buffer inventory that was earmarked to support late-2025 sales, leaving current shelves bare.

According to statements from Intel executives, hyperscaler customers—the massive cloud computing companies driving AI infrastructure buildout—signaled this dramatic shift in requirements throughout the third and fourth quarters of 2025. "Core count was absolutely looking like it would increase, but the units were not expected to increase," one executive explained in a recent earnings call. "And every hyperscaler customer we talked to was signaling that."

Market Impact and Investor Response

The disclosure has sent shockwaves through financial markets, with Intel's stock experiencing sharp declines as investors reassess the company's competitive position in the rapidly evolving AI chip market. The situation is particularly concerning given Intel's ongoing struggles to compete with rivals like NVIDIA and AMD in the AI accelerator space, and TSMC in manufacturing prowess.

The $11.6 billion inventory figure—representing the wrong product mix—underscores the magnitude of the miscalculation and raises questions about capital efficiency and demand forecasting capabilities at a time when precision is critical.

The Road to Recovery

Intel has outlined a multi-pronged recovery strategy:

Prioritizing Data Center Supply: The company is actively shifting internal wafer production away from PC clients toward high-demand server customers, leveraging its integrated manufacturing capabilities to redirect supply chains.

Boosting Factory Efficiency: Intel plans to rely on improved manufacturing yields and throughput to increase chip supply without major new capital expenditures, attempting to squeeze more output from existing facilities.

Timeline Expectations: Management has confirmed that supply improvements should become visible starting in Q2 2026, with expectations for "better than seasonal" growth post-Q1. The recovery trajectory shows gradual improvement through 2026, though the company acknowledges this will be a multi-quarter challenge.

Broader Industry Implications

Intel's predicament highlights the unprecedented volatility in semiconductor demand patterns driven by the AI revolution. The shift from expecting incremental improvements in chip complexity to explosive growth in unit volumes caught even one of the industry's most experienced players off guard.

For investors and industry watchers, Intel's situation serves as a case study in the risks of the current semiconductor landscape: long production lead times, capital-intensive manufacturing, and rapidly shifting technology trends create a perfect storm for supply-demand mismatches.

The question now is whether Intel's recovery plan can execute quickly enough to prevent permanent market share losses to competitors who correctly anticipated the AI-driven demand surge—and whether the company's manufacturing advantages can truly compensate for its strategic miscalculation.

This article is for informational purposes only and should not be considered investment advice. Readers should conduct their own research and consult with financial advisors before making investment decisions.