"You only need 20 great ideas in a lifetime. Most investors won't find even 10."

— Warren Buffett

The Question That Changes Everything

If you could only own 10 stocks for the rest of your life—companies so bulletproof that your grandchildren could inherit them and still get rich—which would you choose?

This isn't a hypothetical parlor game. This is the core philosophy of intelligent investing. While Wall Street tells you to "diversify" across 50 mediocre stocks, the greatest investors in history—Buffett, Munger, Peter Lynch—built their fortunes by concentrating capital in a handful of wonderful businesses they understood deeply and held forever.

But here's the uncomfortable truth: Most companies don't deserve your capital.

Of the 60,000+ publicly traded companies on Earth, only a tiny fraction possess the three traits that define a "forever hold":

An unbreakable moat - A competitive advantage so wide that competitors give up trying

Pricing power - The ability to raise prices without losing customers (inflation becomes profit, not cost)

Irreplaceability - A business model that cannot be replicated, no matter how much money you throw at it

In this article, we're going to identify the only 10 companies on Earth that pass this brutal filter. We've ranked them using the Investment Pyramid—a tier system designed to enforce scarcity and force you to think like Buffett: "Would I use one of my 20 lifetime punches on this?"

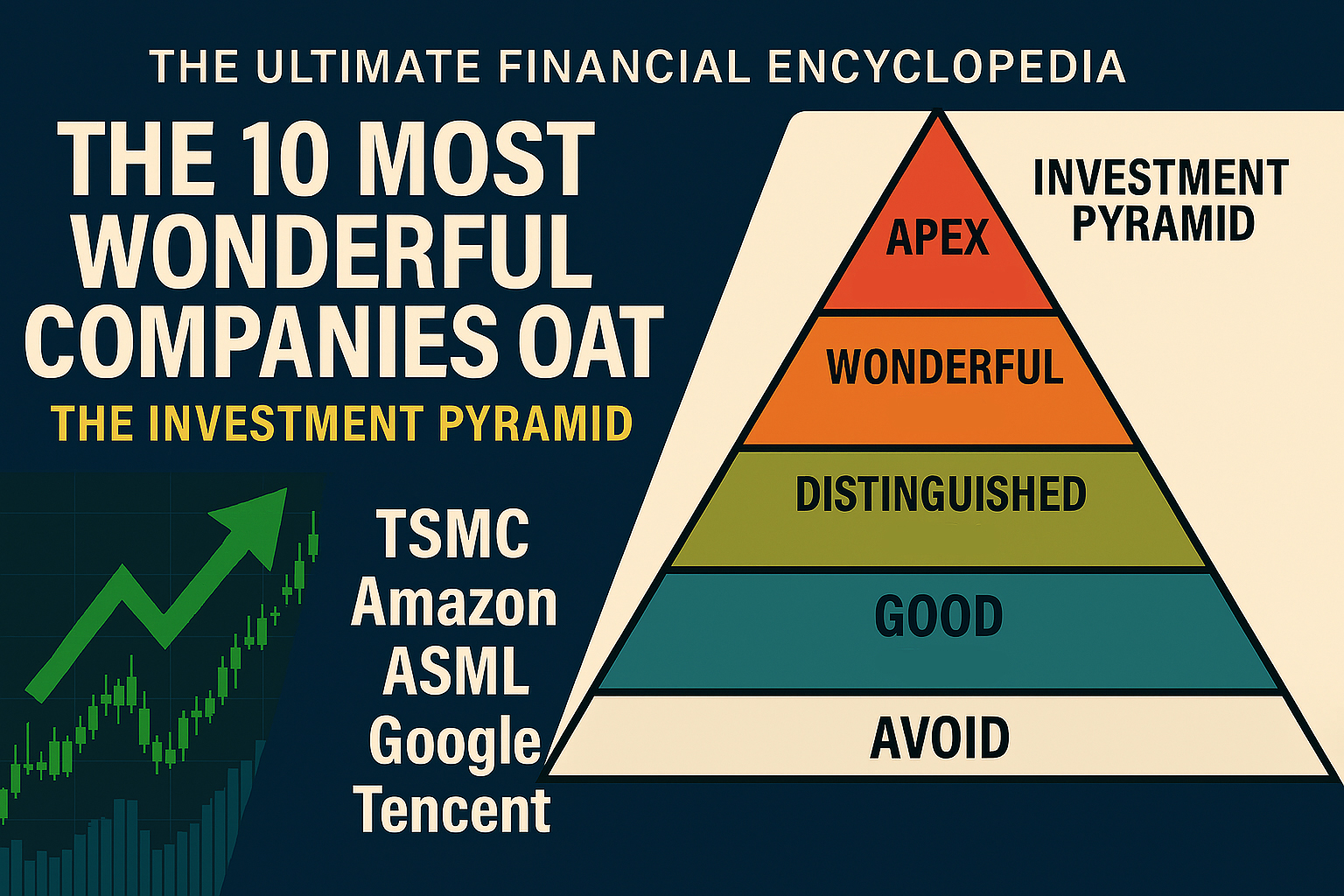

The Investment Pyramid: How We Rank Companies

Before we reveal the Top 10, you need to understand our ranking system. We reject the childish "S/A/B/C/D" tiers borrowed from video games. Instead, we use a pyramid structure that geometrically enforces scarcity:

▲ Tier 0: APEX (1-3 companies)

◆◆ Tier 1: WONDERFUL (5-12 companies)

■■■■■ Tier 2: DISTINGUISHED (15-30 companies)

●●●●●●● Tier 3: GOOD (40-70 companies)

▼▼▼▼▼▼▼▼▼ Tier 4: FAIR (100-200 companies)

✖✖✖✖✖✖✖✖✖ AVOID (∞)Tier 0: APEX - "Cannot Be Replaced by Any Amount of Money"

These are the Nonpareil—the unrivaled. If you gave a competitor $500 billion and 20 years, they still couldn't replicate these businesses. The world cannot function without them.

Criteria:

Global monopoly or duopoly protected by network effects, geography, or accumulated knowledge

Impossible to replicate (would take decades and hundreds of billions)

Zero technological disruption risk on a 20-year horizon

The test: If this company disappeared tomorrow, would civilization collapse? If yes, it's Apex.

Tier 1: WONDERFUL - "The Compounders You Hold Forever"

These are businesses with wide moats that compound intrinsic value over decades. They have real competitors, but their advantages are so strong that competition is economically painful. You buy these and never sell.

Criteria:

Wide moat (brand, switching costs, network effects, scale)

ROIC >15% sustained for 10+ years

Pricing power (can raise prices without losing customers)

Would use a "20-punch card" slot on this

The test: Would I be comfortable holding this for 30 years without checking the price? If yes, it's Wonderful.

Tier 0: APEX - The Two Companies That Rule the World

Only two companies on Earth pass the Apex test. Everything else has a competitor, a technological risk, or a dependency that disqualifies it.

#1: TSMC (Taiwan Semiconductor Manufacturing Company)

Ticker: TSM (NYSE)

Why It's Apex: Process knowledge monopoly. The world cannot function without it.

The Moat: 40 Years of Accumulated Knowledge

TSMC doesn't just make advanced semiconductors—it has 40 years of process knowledge that cannot be bought, stolen, or replicated. Here's why:

Intel, Samsung, and China all have access to the same ASML machines TSMC uses. Yet none of them can match TSMC's performance:

TSMC: 3nm chips at 70-80% yield (70-80% of chips coming off the line work perfectly)

Samsung: 3nm chips at 50-60% yield (loses money on every wafer)

Intel: Stuck at "Intel 7" (equivalent to TSMC's 7nm from 2018)

China (SMIC): Stuck at 7nm with 30-40% yields (and that's using smuggled equipment)

Why the gap? Because TSMC has spent 40 years learning the recipe:

How long to expose silicon to UV light

At what temperature

With what chemical dopants

In what sequence

How to minimize defects in cleanrooms

How to optimize yields through millions of iterations

This knowledge cannot be bought. Even if Intel hired every TSMC engineer, they wouldn't have the institutional memory—the millions of failed experiments that taught TSMC what NOT to do.

The Volume Flywheel

TSMC produces 14 million wafers per year (300mm equivalent).

Samsung produces ~8 million.

Intel produces ~6 million.

Every wafer teaches you something. TSMC has 2x the iteration speed of competitors. When Samsung is debugging their 3nm process on wafer #1,000, TSMC is already on wafer #5,000 and has solved problems Samsung hasn't even encountered yet.

This creates a compounding moat: More customers → More volume → Better yields → Lower costs → More customers.

The "Taiwan Risk" Is Actually a Moat

Critics say: "But what if China invades Taiwan?"

This is exactly why TSMC is Apex. If Taiwan disappeared tomorrow:

iPhone production stops (Apple has no alternative for 3nm A17 chips)

NVIDIA H100 production stops (no one else can make 5nm AI GPUs at scale)

Global semiconductor supply collapses by 50%+

The world economy grinds to a halt

TSMC's Arizona and Japan fabs: Will make 4nm chips by 2025-2026, but they're still 1-2 generations behind Taiwan's 2nm fabs. The cutting edge remains in Taiwan.

The US knows this. That's why the CHIPS Act gave TSMC $6.6 billion to build US fabs. That's why Biden said the US would defend Taiwan militarily. TSMC isn't just a company—it's critical infrastructure for Western civilization.

The Customer Lock-In

Apple: Designed their M-series chips specifically for TSMC's 3nm process. Switching to Samsung would require 2+ years of re-design.

NVIDIA: H100 GPUs are optimized for TSMC's 5nm CoWoS (Chip-on-Wafer-on-Substrate) packaging. Can't just move to Intel.

AMD: Entire Ryzen/EPYC roadmap is TSMC-dependent.

TSMC isn't a vendor. It's a partner. Apple, NVIDIA, AMD, and Qualcomm design chips for TSMC's processes, not the other way around.

Why TSMC Is Apex, Not Just Wonderful

The test: Could anyone replicate TSMC with unlimited money and time?

Answer: No. China has spent $150+ billion over a decade trying to build a TSMC competitor (SMIC). They're still 5+ generations behind. Intel spent $100+ billion trying to catch up. They're 3-4 years behind and bleeding talent.

TSMC's moat isn't just technical—it's temporal. You can't compress 40 years of learning into 10 years, no matter how much you spend.

Verdict: ✅ Tier 0 (APEX). The world cannot function without TSMC. It is irreplaceable.

#2: Amazon (AMZN)

Ticker: AMZN (NASDAQ)

Why It's Apex: Infrastructure moat. $200+ billion and 15 years to replicate.

The Dual Moat: AWS + Fulfillment Network

Amazon isn't one business—it's two separate monopolies that compound each other:

AWS (Amazon Web Services): 32% of the global cloud market. $90+ billion in annual revenue. 30% operating margins.

Fulfillment Network: 1,500+ warehouses globally, positioned algorithmically for 1-2 day delivery to 90% of the US population.

Both moats are physical infrastructure that cannot be replicated economically.

AWS: The Invisible Monopoly

Who uses AWS?

Netflix (streams on AWS)

Spotify (runs on AWS)

Airbnb (built on AWS)

90+ of the Fortune 100 companies

Why can't competitors catch up?

Customer lock-in: Once a company builds its infrastructure on AWS (using EC2 instances, S3 storage, Lambda functions, RDS databases), switching to Azure or Google Cloud requires re-architecting the entire tech stack. The switching cost is millions of dollars and 12-18 months of engineering time.

Network effects: AWS has 200+ services (databases, AI/ML tools, analytics, IoT, etc.). Microsoft Azure has ~100. Google Cloud has ~60. The gap is widening, not shrinking.

First-mover advantage: AWS launched in 2006. Microsoft Azure launched in 2010 (4 years late). Google Cloud launched in 2011 (5 years late). By the time they entered, AWS had already locked in enterprise customers and built services that competitors are still trying to copy.

The Fulfillment Network: The Physical Moat

Amazon's warehouse network:

1,500+ fulfillment centers globally (US, Europe, Asia)

Algorithmically positioned for maximum coverage (1-2 day delivery to 90% of US)

400+ million square feet of warehouse space (equivalent to 7,000 football fields)

To replicate this:

Cost: $200+ billion (land, construction, automation, inventory)

Time: 15+ years (zoning, permits, hiring, logistics optimization)

Coordination: You'd need to build everything simultaneously (one warehouse is useless without the network)

Walmart tried. They spent $10+ billion on e-commerce and logistics (2016-2023). They're still 10 years behind Amazon in delivery speed and selection.

Target tried. They partnered with Shipt. Still can't match Amazon's 1-day delivery on millions of items.

Why? Because Amazon didn't just build warehouses—they built an algorithm:

Where to place warehouses (proximity to population centers)

What inventory to stock in each warehouse (predictive analytics)

How to route packages (minimizing miles traveled)

How to automate picking/packing (robotics, AI)

This knowledge took 20+ years to accumulate. You can't buy it.

The Third Moat: The Marketplace Flywheel

Amazon's 3P (third-party) marketplace:

60% of items sold on Amazon are from third-party sellers (not Amazon itself)

2 million+ active sellers globally

$200+ billion in 3P sales (2023)

Why this matters:

Sellers pay Amazon 15% of every sale (plus FBA fees if they use Amazon's warehouses)

More sellers → More selection → More customers → More sellers (flywheel)

Network effects: If you're a seller, you MUST be on Amazon. If you're a customer, Amazon has everything you need.

This creates a moat within a moat: Even if a competitor built a warehouse network, they'd need to convince 2 million sellers to list on their platform. Why would sellers do that when Amazon already has 300+ million customers?

Why Amazon Is Apex, Not Just Wonderful

The test: Could anyone replicate Amazon with unlimited money and time?

Answer: Economically, no. You'd need:

$200+ billion for warehouses

15+ years to build the network

Another $50+ billion to build AWS-equivalent cloud services

Another 10+ years to convince enterprise customers to switch

The willingness to lose money for a decade (Amazon didn't turn a profit until 2015—18 years after founding)

No company has this combination of capital, patience, and execution. Walmart has the capital but not the tech DNA. Google has the tech DNA but not the logistics expertise. Alibaba has both in China, but can't replicate in the West.

Verdict: ✅ Tier 0 (APEX). Amazon's infrastructure moat is physically and economically irreplaceable.

Tier 1: WONDERFUL - The 8 Companies You Hold Forever

These are businesses with wide moats that compound over decades. They face real competition, but their advantages are so strong that competing is economically painful. You buy these with "20-punch card" conviction and hold forever.

#3: ASML (ASML Holding)

Ticker: ASML (NASDAQ)

Why It's Wonderful: EUV lithography monopoly. Only company on Earth that can make the machines that make advanced chips.

The Monopoly: Extreme Ultraviolet (EUV) Lithography

To make chips smaller than 7nm, you need EUV (Extreme Ultraviolet) lithography machines. These machines cost $380 million each and use 13.5nm wavelength light to etch transistors onto silicon wafers.

Only one company on Earth can make EUV machines: ASML.

Who needs EUV?

TSMC (has ~50 EUV machines)

Samsung (has ~20 EUV machines)

Intel (has ~10 EUV machines, ordered more)

Why can't anyone else make EUV?

The Zeiss Moat: ASML owns 24.9% of Carl Zeiss SMT (German optics company). Zeiss makes the mirrors for EUV machines—mirrors so precise they're polished to within 1/1000th the width of a human hair.

Zeiss's corporate structure prevents full acquisition (German foundation laws). ASML has exclusive access to Zeiss optics. No one else can buy them.

The Supply Chain Moat: ASML doesn't make EUV machines alone. It orchestrates 800+ suppliers:

Zeiss (Germany): Optics

Cymer (USA, owned by ASML): Light sources

TRUMPF (Germany): Lasers

VDL (Netherlands): Precision mechanics

To replicate ASML, you'd need to replicate this entire supply chain. China has been trying for 10+ years with SMEE (Shanghai Micro Electronics Equipment). They're still stuck at 28nm DUV (Deep Ultraviolet) lithography—3 generations behind.

Why ASML Is NOT Tier 0 (Apex)

The China Risk: If China cracks EUV in 10-15 years, ASML's monopoly collapses.

The Dependency Risk: ASML is a tool supplier, not the craftsman. It sells machines to TSMC, Samsung, and Intel. If any of these customers disappear (e.g., geopolitical conflict), ASML loses revenue.

TSMC is the craftsman: Even with ASML's machines, Intel and Samsung can't match TSMC's yields. ASML's machines are necessary but not sufficient for making advanced chips.

Verdict: ✅ Tier 1 (WONDERFUL). ASML has a 10-15 year monopoly, but it's not "impossible to replicate forever" like TSMC.

#4: Microsoft (MSFT)

Ticker: MSFT (NASDAQ)

Why It's Wonderful: Enterprise lock-in across three moats: Azure, Office 365, and Windows.

The Triple Moat

Microsoft isn't one business—it's three separate moats that compound:

Azure (cloud): 23% market share, catching up to AWS (32%). $70+ billion annual revenue.

Office 365 (productivity): 345 million paid subscribers. Word, Excel, PowerPoint, Outlook, Teams.

Windows (operating system): 73% of desktop OS market share. Enterprise runs on Windows.

Each moat reinforces the others:

Companies use Windows desktops → locked into Office 365 → deploy cloud apps on Azure (because it integrates seamlessly with Windows/Office)

The Enterprise Lock-In

Try getting a Fortune 500 company to migrate away from Microsoft:

Migrate from Windows to Linux? Impossible. Enterprise software (SAP, Oracle, proprietary apps) runs on Windows.

Migrate from Office 365 to Google Workspace? Economically insane. Retraining 10,000+ employees on new productivity tools costs millions. Excel macros break. PowerPoint templates don't transfer.

Migrate from Azure to AWS? Requires re-architecting entire cloud infrastructure. Takes 12-18 months and millions in engineering costs.

Switching costs are so high that companies don't even try.

Why Microsoft > NVIDIA

Microsoft vs NVIDIA:

NVIDIA depends on TSMC (if TSMC disappeared, NVIDIA's chips can't be made)

Microsoft owns its entire stack (cloud, software, OS)

NVIDIA's moat is execution; Microsoft's moat is lock-in

Microsoft's moat is enterprise software

Verdict: ✅ Tier 1 (WONDERFUL). Microsoft's enterprise lock-in is the strongest moat in software.

#5: NVIDIA (NVDA)

Ticker: NVDA (NASDAQ)

Why It's Wonderful: CUDA ecosystem + AI infrastructure moat. But AMD/Google compete, and NVIDIA depends on TSMC.

The CUDA Moat

CUDA (Compute Unified Device Architecture) is NVIDIA's software platform for GPU computing. Launched in 2006, it's now the de facto standard for:

AI/ML training (PyTorch, TensorFlow run on CUDA)

Scientific computing (molecular dynamics, climate modeling)

Rendering (Pixar, ILM use CUDA for CGI)

Switching costs: If you're an AI researcher and you've written 100,000 lines of CUDA code, switching to AMD's ROCm requires rewriting everything. That's 6-12 months of engineering time.

Developer lock-in: 4+ million developers use CUDA. They've built libraries, tools, and workflows around it. AMD has ~100,000 developers on ROCm.

The AI Infrastructure Moat

NVIDIA's H100/H200 GPUs power the AI boom:

OpenAI (GPT-4): Trained on 10,000+ NVIDIA A100 GPUs

Meta (Llama 3): Trained on 16,000+ H100 GPUs

Google (Gemini): Uses Google TPUs, but also buys NVIDIA GPUs for flexibility

Why H100/H200 dominate:

Performance: 3-4x faster than AMD's MI300X in AI training

Software ecosystem: CUDA, cuDNN, TensorRT libraries are mature

Availability: TSMC makes NVIDIA chips at 70%+ yields; Samsung makes AMD chips at 50% yields

Why NVIDIA Is NOT Tier 0 (Apex)

The TSMC Dependency: NVIDIA doesn't manufacture chips. It designs them and pays TSMC to make them. If TSMC disappeared, NVIDIA's H100/H200 GPUs can't be made at scale (Samsung's yields aren't good enough).

The Competition: AMD's MI300X is catching up. Google's TPU v5 exists (closed ecosystem, but proves CUDA isn't essential). Intel's Gaudi 3 is trying (and failing, but they're trying).

The Commoditization Risk: In 10 years, AI chips might be like RAM—standardized, low margins. NVIDIA's moat is execution (being first and best), not impossibility (like TSMC's process knowledge).

Verdict: ✅ Tier 1 (WONDERFUL). NVIDIA is the best AI infrastructure company today, but it's not irreplaceable forever.

#6: Google (Alphabet - GOOGL)

Ticker: GOOGL (NASDAQ)

Why It's Wonderful: Search monopoly (92% market share) + Android (71% mobile OS) = data flywheel that compounds.

The Search Monopoly

Google Search: 92% market share globally. 8.5 billion searches per day.

Why can't Bing/DuckDuckGo compete?

The Data Flywheel:

More searches → More data on user intent

More data → Better search results (algorithm learns what people want)

Better results → More users → More searches (loop)

Google has 25+ years of search data. Bing has 15 years. DuckDuckGo has 5 years. The quality gap is unbridgeable without decades of data.

The Android Moat

Android: 71% of mobile OS market share globally (iOS is 28%).

Why this matters:

Android comes pre-loaded with Google Search, Chrome, Gmail, Maps, YouTube

Default placement = monopoly. 95% of Android users never change their default search engine.

This gives Google billions of searches per day from mobile (where most searches now happen)

Why Google Is Tier 1 (Wonderful), Not Tier 0 (Apex)

Google represents the pinnacle of digital infrastructure—a self-reinforcing ecosystem of search, Android, YouTube, and AI that has compounded dominance for two decades. Its capital allocation is exemplary: search profits ($80B+ annual FCF) are relentlessly reinvested into cloud, AI (Gemini), and moonshots, ensuring the company evolves rather than ossifies. Unlike many tech giants, Google anticipates disruption and builds through it.

Yet Tier 0 demands a stricter test: structural irreplaceability—the inability to be replicated even with infinite capital and time.

Google fails this test not because it is weak, but because alternatives do exist at scale:

China functions without Google: Baidu serves 1B+ users; the entire Chinese internet ecosystem thrives independently. This proves search infrastructure can be rebuilt regionally—a luxury TSMC (no alternative for 3nm chips) or Amazon (no alternative for global logistics density) do not have.

The web is not owned by Google: Unlike TSMC's fabs or Amazon's warehouses, Google indexes content it does not control. Publishers could collectively redirect traffic (as Australia's news code demonstrated). Its moat is behavioral (habit) and algorithmic—not physical or knowledge-based.

Competition persists at the edges: Yandex (Russia), Naver (Korea), DuckDuckGo (privacy), and emerging AI-native interfaces (Perplexity) nibble at the margins. They haven't displaced Google—but their existence proves the moat is wide, not unbreachable.

This is not a weakness—it is the definition of Tier 1 (Wonderful): a business so dominant that challengers fail repeatedly, yet theoretically replaceable given enough time, capital, and geopolitical fragmentation. Google's genius lies in making replacement economically irrational for two decades and counting. But unlike TSMC's 40 years of tacit process knowledge or Amazon's $200B+ physical network, Google's advantage could be rebuilt—just at staggering cost and time.

Tier 0 belongs to infrastructure the world cannot function without.

Tier 1 belongs to companies that make the world function better—and Google sits proudly at its apex.

#7: Tencent (TCEHY)

Ticker: TCEHY (OTC, listed in Hong Kong as 0700.HK)

Why It's Wonderful: WeChat super-app. 1.3 billion users. The entire Chinese internet runs on Tencent.

The WeChat Monopoly

WeChat isn't just a messaging app—it's the entire Chinese internet in one app:

Messaging: 1.3 billion monthly active users (everyone in China uses WeChat)

Payments: WeChat Pay (50% of China's mobile payment market, competing with Alipay)

Social media: Moments (like Facebook feed)

E-commerce: Mini-programs (shop inside WeChat without leaving the app)

Government services: Pay taxes, renew licenses, book hospitals—all inside WeChat

Transportation: Hail taxis, buy train tickets

Food delivery: Order meals

WeChat is so embedded in Chinese life that NOT using it is like not having a phone number.

The Network Effects

Why can't anyone compete with WeChat?

Social graph lock-in: Everyone you know is on WeChat. Switching to a competitor means losing contact with 1.3 billion people. This is the ultimate network effect.

Mini-programs: 4+ million mini-programs (lightweight apps) run inside WeChat. Businesses build for WeChat because that's where the users are. Users stay on WeChat because that's where the services are.

Government integration: The Chinese government uses WeChat for official communications. You can't opt out.

The Gaming Moat

Tencent is the world's largest gaming company:

Owns Riot Games (League of Legends, Valorant)

Owns 40% of Epic Games (Fortnite, Unreal Engine)

Owns Supercell (Clash of Clans, Clash Royale)

Publishes Honor of Kings (most profitable mobile game ever, $10+ billion cumulative revenue)

Why this matters: Gaming is a recurring revenue business. Players spend money on skins, battle passes, in-game currency. League of Legends has generated $20+ billion since 2009.

Why Tencent Is NOT Tier 0 (Apex)

The CCP Risk: The Chinese Communist Party can destroy Tencent overnight if it wants. See what happened to Alibaba:

Jack Ma criticized Chinese regulators (October 2020)

CCP canceled Ant Group's $37B IPO (November 2020)

Alibaba fined $2.8 billion (April 2021)

Jack Ma disappeared for 3 months

Tencent operates at the pleasure of the CCP. If Xi Jinping decides WeChat is a "threat to social stability," the entire business could be nationalized.

The Teen Gaming Crackdown: In 2021, China limited minors to 3 hours of gaming per week. This hurt Tencent's gaming revenue growth.

Verdict: ✅ Tier 1 (WONDERFUL). WeChat's moat is as strong as Google's in China, but CCP risk is existential.

#8: Apple (AAPL)

Market Cap: ~$3.4 trillion (as of Feb 2026)

Ticker: AAPL (NASDAQ)

Why It's Wonderful: Ecosystem lock-in (iMessage, AirPods, iCloud, Services). But phones are competitive (Samsung exists).

The Ecosystem Moat

Apple doesn't sell phones. It sells an ecosystem you can't leave.

The lock-in starts with iMessage:

Green bubble stigma: If you have an Android, your messages show up as green bubbles in group chats. You're excluded from reactions, high-res photos, and read receipts.

Social pressure: Among US teens, 87% use iPhones (2023 survey). If you switch to Android, you're socially ostracized.

Then it compounds:

AirPods: Seamless pairing with iPhone/iPad/Mac. Switch to Android and you lose this.

Apple Watch: Health data (heart rate, sleep tracking, ECG) syncs with iPhone. Switch to Android and you lose years of health history.

iCloud: Photos, contacts, notes stored in iCloud. Switch to Android and you need to migrate everything (painful).

App Store purchases: You've spent $500+ on apps over the years. Switch to Android and you re-buy everything.

Switching cost: $2,000+ in devices + data migration + social stigma.

The Services Moat

Apple's fastest-growing business isn't hardware—it's Services:

App Store: $85 billion in annual revenue (2023). Apple takes 30% of every app sale + in-app purchase.

iCloud: $14 billion in annual revenue. You pay $0.99/month for 50GB, $2.99/month for 200GB.

Apple Music: 100+ million subscribers at $10.99/month.

Apple TV+: 25+ million subscribers (bundled with Apple One).

Services revenue: $85+ billion in 2023, growing 10% YoY. Gross margin: 70%+ (vs 36% for hardware).

This is the "razor-and-blades" model: Sell iPhones at moderate margins (36%), then extract high-margin recurring revenue from Services (70%) forever.

Why Apple Is NOT Tier 0 (Apex)

The Hardware Commoditization Risk: Samsung, Xiaomi, and Huawei make phones as good as iPhones (in specs). The camera on a Samsung Galaxy S24 Ultra is arguably better than iPhone 15 Pro Max. The chip in a Xiaomi 14 Ultra (Snapdragon 8 Gen 3) benchmarks close to Apple's A17 Pro.

What keeps Apple ahead? Ecosystem lock-in, not hardware superiority.

The China Risk: iPhone sales in China dropped 24% YoY (Q1 2024) due to Huawei's comeback. If China bans iPhones (in retaliation for US chip sanctions), Apple loses 19% of revenue.

The Next Growth Driver Is Unclear:

Vision Pro flopped ($3,500 headset, selling <500K units in year 1)

Apple Car canceled (after 10 years and $10+ billion spent)

Foldable iPhones? Maybe, but Samsung has a 5-year head start

Verdict: ✅ Tier 1 (WONDERFUL). Apple's ecosystem moat is real, but hardware commoditization + China risk keep it out of Tier 0.

#9: Ferrari (RACE)

Market Cap: ~$85 billion (as of Feb 2026)

Ticker: RACE (NYSE)

Why It's Wonderful: Only automaker where cars appreciate. 76-year brand moat + Veblen pricing power.

The Appreciation Moat

Ferrari is the only automaker in history where cars consistently appreciate:

Ferrari F40 (1987-1992): Cost $400K new → Worth $2-3 million today (5-7x appreciation)

Ferrari Enzo (2002-2004): Cost $650K new → Worth $3-4 million today (5-6x appreciation)

LaFerrari (2013-2016): Cost $1.4M new → Worth $5-7 million today (4-5x appreciation)

Why does this happen?

Structural scarcity: Ferrari intentionally produces fewer cars than demand. They make ~14,000 cars per year and could easily make 50,000 (like Porsche), but they don't. This creates perpetual scarcity.

Veblen pricing: The more expensive a Ferrari gets, the more people want it. A $500K Ferrari is a status symbol. A $3M Ferrari is a flex. A $7M LaFerrari is proof you're in the top 0.001%.

Brand waitlists: To buy a new LaFerrari, you needed to:

Already own 5+ Ferraris

Be invited by Ferrari (they choose you, not the other way around)

Wait 2+ years

This isn't a car company. It's a luxury asset class.

The Brand Moat (76 Years)

Ferrari was founded in 1947. 76 years of racing heritage (Formula 1 dominance), Italian craftsmanship, and celebrity ownership (Steve McQueen, Jay Leno, Floyd Mayweather) have created a brand that cannot be replicated.

Competitors tried:

McLaren: Made the P1 (hypercar, limited to 375 units). It appreciated 2x, then crashed 50% in 2020. Not consistent.

Lamborghini: Aventador SVJ appreciated briefly, but most Lambos depreciate.

Pagani: Zonda appreciated, but production is tiny (~40 cars/year). Not scalable.

Bugatti: Chiron depreciates 30-40% the moment you drive it off the lot.

No other automaker has Ferrari's combination of scarcity + brand + racing heritage.

Why Ferrari Is NOT Tier 0 (Apex)

Taste Dependency: Luxury is taste-dependent. What if Gen Z decides Ferraris are "cringe" in 2040?

Historical precedent:

Burberry was the pinnacle of British luxury in 1990. By 2015, it was "tacky" (worn by soccer hooligans). Brand collapsed 50%.

Gucci nearly went bankrupt in 2000 (pre-Tom Ford). Revived by creative direction, proving luxury brands can die.

The EV Transition Risk: Ferrari's first EV launches in 2025. Can they maintain brand mystique in EVs?

Teslas don't appreciate (Model S from 2012 is worth $20K, down 80%)

Rivians don't appreciate

Lucids don't appreciate

If Ferrari's EVs depreciate like normal cars, the entire "appreciating asset" moat collapses.

Verdict: ✅ Tier 1 (WONDERFUL). Ferrari's brand moat is 76 years strong, but luxury is taste-dependent and EV transition is risky.

#10: Visa & Mastercard (V / MA)

Market Cap: Visa ~$615B, Mastercard ~$475B (as of Feb 2026)

Tickers: V (NYSE), MA (NYSE)

Why They're Wonderful: Payment network effects. But regional moat (weak in Germany/China). CBDC risk is distant.

The Network Effects Moat

Visa and Mastercard don't issue credit cards. They run the payment rails.

How it works:

You swipe your Visa card at Starbucks

Starbucks's bank (merchant acquirer) sends the transaction to Visa

Visa routes it to your bank (card issuer)

Your bank approves the charge

Visa settles the transaction between banks

Visa takes 0.1-0.3% of the transaction as a fee

This happens in 400 milliseconds. Globally. For 270+ billion transactions per year.

The duopoly: Visa and Mastercard control 90%+ of global card payment volume. No one else can compete because of network effects:

Merchants accept Visa/Mastercard because consumers use them

Consumers use Visa/Mastercard because merchants accept them

Banks issue Visa/Mastercard because both sides demand them

This is a three-sided network effect (consumers, merchants, banks). Breaking it requires getting all three sides to switch simultaneously—economically impossible.

The Toll Booth Business Model

Visa and Mastercard are toll booths on the global economy:

Every time money moves electronically, they take a cut (0.1-0.3%)

They don't take credit risk (banks do)

They don't handle customer service (banks do)

They just process transactions and collect fees

Operating margins: 60-65% (among the highest in the world).

This is why Buffett called it "the best business model in the world."

Why Visa/Mastercard Are NOT Tier 0 (Apex)

The Regional Moat Problem: Visa/Mastercard are dominant in the US and UK, but not globally:

Germany: Girocard (German debit system) processes 5.8 billion transactions/year. Visa/Mastercard are used for online/international, but cash + Girocard dominate in-store.

China: UnionPay (90% of card transactions domestically). Alipay/WeChat Pay bypass cards entirely (QR code payments).

India: UPI (Unified Payments Interface) processes 12+ billion transactions/month with zero fees. Visa/Mastercard are becoming irrelevant.

Brazil: Pix (instant bank transfers) launched in 2020, now processes 3+ billion transactions/month. Free, instant, no cards needed.

The CBDC Threat: Central Bank Digital Currencies could bypass card networks entirely. If the Federal Reserve launches a digital dollar, consumers could pay directly from Fed accounts (no Visa/Mastercard needed).

Timeline: 10-15 years away, but the threat is real.

Verdict: ✅ Tier 1 (WONDERFUL). Visa/Mastercard's network effects are strong in the US/UK, but regional moat issues + CBDC risk keep them out of Tier 0.

The Investment Strategy: How to Use This Top 10

Now that you know the only 10 companies that matter, here's how to actually build a portfolio around them:

Strategy 1: The 20-Punch Card Portfolio (Concentrated)

Philosophy: Buy 3-5 companies from this list and hold forever.

Allocation example (for $100,000):

40%: TSMC + Amazon (Tier 0 Apex) = $40,000

40%: ASML + Microsoft + NVIDIA (Tier 1 infrastructure) = $40,000

20%: Google + Apple (Tier 1 consumer moats) = $20,000

Why this works:

You're betting on infrastructure (TSMC, Amazon, ASML, MSFT, NVDA) that the world cannot function without

You're diversified across semiconductors, cloud, software, and AI

You're holding "forever" businesses that compound for decades

Risk: Concentration. If TSMC or Amazon stumbles, you feel it. But if you're confident in the moat (and we are), this is how you get rich.

Strategy 2: The Lazy Winner (Index + Top 3)

Philosophy: Own the S&P 500 for diversification, overweight the Top 3.

Allocation example (for $100,000):

50%: S&P 500 index fund (VOO or SPY) = $50,000

30%: TSMC + Amazon (Tier 0) = $30,000

20%: ASML (Tier 1, highest conviction) = $20,000

Why this works:

S&P 500 gives you exposure to all 500 largest US companies (safety)

Overweighting TSMC/Amazon/ASML gives you outsized returns if they continue dominating

Less risky than pure concentration, but still better than vanilla index investing

Strategy 3: The Geographic Hedge

Philosophy: Diversify across US, Europe, China, and Taiwan.

Allocation example (for $100,000):

US (50%): Amazon, Microsoft, NVIDIA, Apple = $50,000

Taiwan (20%): TSMC = $20,000

Europe (15%): ASML, Ferrari = $15,000

China (15%): Tencent = $15,000

Why this works:

Protects against US-specific risks (recession, regulation)

Protects against China-Taiwan geopolitical risk (you own both sides)

Captures global growth

The Ultimate Lesson: Quality Over Quantity

Wall Street tells you to "diversify" across 50 stocks. They're wrong.

Buffett's Berkshire Hathaway: 70%+ of its equity portfolio is in the top 5 holdings (Apple, Bank of America, American Express, Coca-Cola, Chevron).

Bill Gates (when he left Microsoft's board in 2020): 50%+ of his wealth was still in Microsoft stock (after 20+ years of "diversification").

The Walton family (Walmart founders): 50%+ of their $250 billion fortune is still in Walmart stock.

The pattern: The richest people on Earth got rich by concentrating in a few wonderful businesses and holding forever.

You don't need 50 stocks. You need 3-5 great ideas and the courage to bet big on them.

Your Next Steps: The 20-Punch Card Action Plan

Pick 3-5 companies from this Top 10 that you understand deeply. Can you explain their moat to a 10-year-old? If yes, proceed. If no, study more.

Calculate their Fair Value using DCF (Discounted Cash Flow). We'll teach you this in a future article, but the principle is simple: A business is worth the present value of all its future cash flows.

Wait for Mr. Market's panic. These companies don't go on sale often, but when they do (2020 COVID crash, 2022 tech selloff), buy aggressively.

Hold for 20+ years. Ignore the daily noise. Ignore the "analysts" telling you to sell. Trust the moat.

Reinvest dividends. Compounding is the eighth wonder of the world. Don't interrupt it.

The Final Truth: There Are Only 10

Of the 60,000+ publicly traded companies on Earth, only 10 pass the brutal filter of:

Unbreakable moat

Pricing power

Irreplaceability

2 are Apex (TSMC, Amazon). The world cannot function without them.

8 are Wonderful (ASML, Microsoft, NVIDIA, Google, Tencent, Apple, Ferrari, Visa/Mastercard). You hold them forever.

Everything else is noise.

Your job isn't to own 50 stocks. Your job is to find the 3-5 companies from this list that you understand, buy them when Mr. Market panics, and hold them while the world compounds wealth for you.

"If you aren't willing to own a stock for ten years, don't even think about owning it for ten minutes."

— Warren Buffett

Welcome to the Top 10. Now go build your fortune.